The Financing Process

Demystifying Home Loans

The home loan process can feel overwhelming

By collaborating with a trusted lender and remaining informed through every step of the process, from pre-approval to closing, you can have a significantly more comfortable experience. You’ll want to consult with a mortgage specialist (or two) to find a professional who you are confident will provide you with the best care. To get an idea of what to expect, review the following home loan process steps.

Trust the Service and Experience

Kip Painter leads ONE Presidential Mortgage’s Richmond market with a strong foundation built on two decades of experience in the mortgage industry. What drives him most is the opportunity to build meaningful relationships through every transaction, support his community, and help clients reach their homeownership goals.

Kip’s approach is rooted in connection—he believes the mortgage process is not just about numbers, but about people. His passion for fostering trust and delivering results has made him a respected leader and resource in the Richmond area.

Outside of work, Kip stays busy with his wife and three children. Whether they’re at a track meet, enjoying a day at the beach, or spending time at church, the Painter family is always on the move. Fitness is a big part of their lives, and weekends often revolve around cross country and track competitions. Their two golden doodles, Luna and Indy, are always close behind.

Whether you’re a borrower, Realtor, or fellow loan officer, Kip brings dedication, integrity, and a deep commitment to every relationship—making him a valuable asset to both his team and the Richmond community.

Kip Painter | Area Leader

ONE PRESIDENTIAL MORTGAGE

NMLS 1021601

3406 W Clay St

Richmond

VA 23230

(804) 347-3250

kip.painter@onepresidentialmtg.com

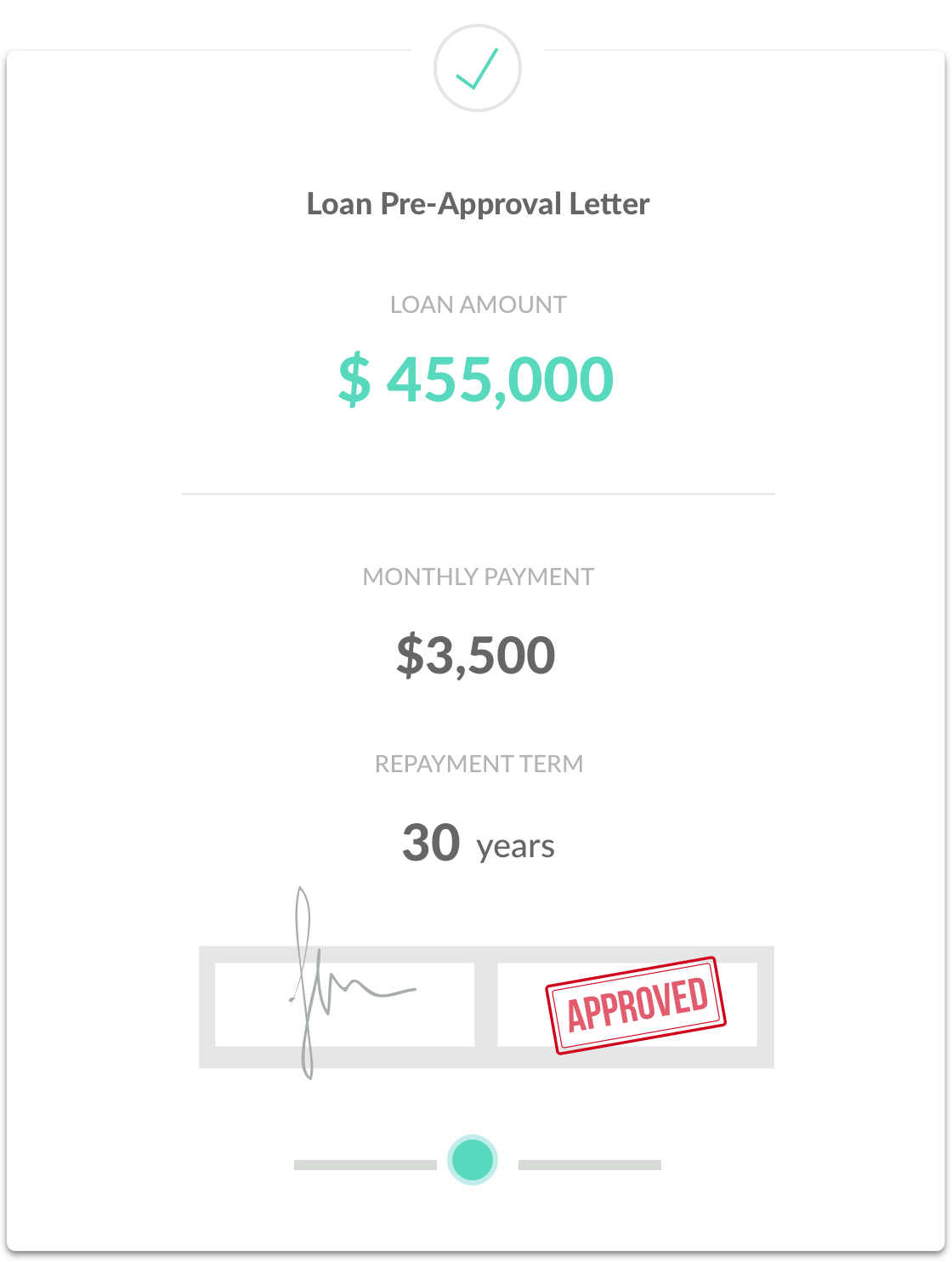

Step One:

Get pre-approval

Before you start looking for a home to buy, it’s wise and proactive to meet with a lender to get pre-approved for a loan amount. Offers accompanied by a pre-approval letter are stronger and will stand out, especially when the seller is receiving multiple offers.

To gain pre-approval, your preferred lender will gather information about income, assets, and debts to help determine how much you can borrow. This includes gathering a credit report, W-2 forms, pay stubs, federal tax returns, and recent bank statements.

There are a variety of home loan programs offering different advantages depending on your unique needs and preferences. Your preferred lender can go over the specifics of each to ensure you find a loan option that best aligns with your needs.

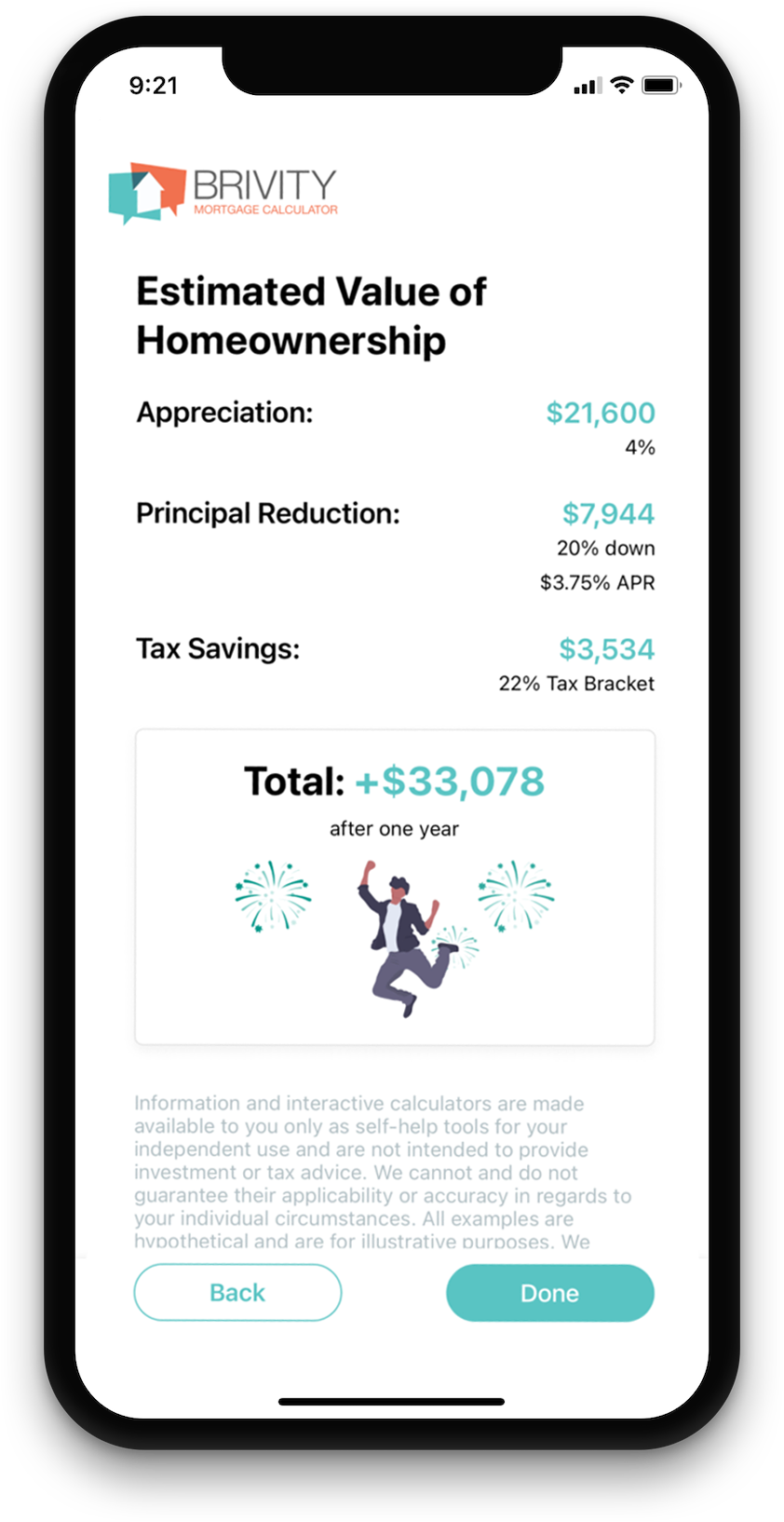

Estimate Your Monthly Payment

Estimate your mortgage payment, including the principal and interest, taxes, insurance, HOA, and Private Mortgage Insurance.

Price

Annual Tax

Loan Term (Years)

Down Payment %

Interest Rate %

Monthly HOA

Monthly Insurance

$3,198.20

Estimated Monthly Payment

Principal

$2,398.20

(75.0%)Taxes

$500.00

(15.6%)HOA

$100.00

(3.1%)Insurance

$200.00

(6.3%)Step Two:

Find the best loan

Collaborating with a top-notch local loan officer will ensure you have access to competitive rates and programs that best fit your individual needs. Take the first step by completing this form to get connected today!

Step Three:

Application and Processing

When you find the perfect property and your offer is accepted, your lender will help you complete a full mortgage loan application, discuss down payment options, and explain any related fees.

Then, your application is submitted for processing where the documents are reviewed. Your lender will also order a home appraisal and a property title search.

The next part of the application process involves sending everything to an underwriter who will review and approve the entire loan package to make sure it meets all compliance regulations.

It is not unusual to receive requests for additional documentation or clarification during this phase of the application process.

Step Four:

Signing and Finalizing the deal

Once your loan is approved, you’ll need to set up homeowners insurance.

Your documents will be sent to the title company and the closing will be scheduled for you to sign the necessary paperwork and pay any additional costs to complete the purchase of your new home.

After the loan goes through the required recording process, the purchase is complete, and you officially own your new home!